Is there a new debt crisis on the horizon?

The US Federal Reserve governor, Jerome Powell, stated in the recent Jackson Hole meetings of global central bankers that the US economy is doing well at present and confirmed the continuation of interest-rate hikes in the foreseeable future.

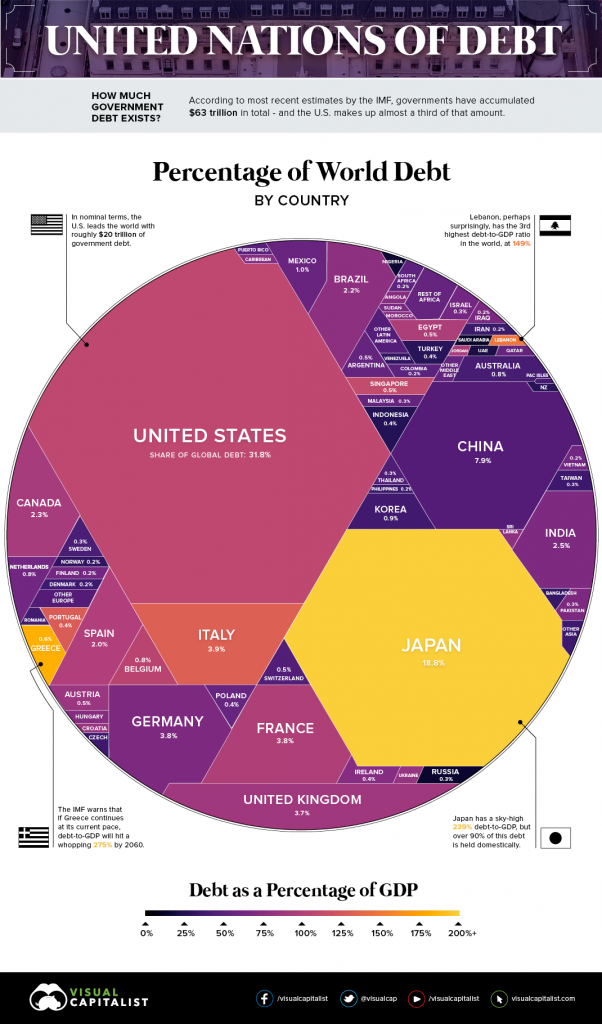

Chinese debt has increased from 160% of GDP in 2008 to 260% in 2016.

A new debt crisis on the horizon?

Even though such a stance is probably already priced in by the global financial market and did not stir up too much of a global ripple, what happened in Venezuela and Turkey earlier this year still unavoidably remind global policymakers and investors of how fragile certain economies may become in light of the US’s interest-rate hike cycle.

After all, the 1998 south-east Asian financial crisis and 2008 global financial crisis are not that distant, historically speaking; coincidentally enough, both years end with the number 8, significant in some oriental cultures, just as this year does. Therefore, even a slight hint from the Federal Reserve about future interest rate trends would keep investors all over the globe on their toes.

Historically, the cycle of interest rate hikes by the Federal Reserve has been a key factor in the pricing and volatility of relatively risky and illiquid assets, such as fixed income securities issued and traded in emerging markets. If anything, recent turmoil in the global debt, equity and currency markets once again questions the viability and sustainability of the economic growth in some emerging economies and emerging financial markets.

If history can be a useful benchmark, three types of risks may emerge in emerging economies in response to interest rate hikes:

1. Capital flight

The most obvious and direct source of the risk emerging market economies face is capital flight. A hike by the Federal Reserve reduces the interest rate gap between the US and emerging economies, and increases the appeal of US securities. If a large amount of international and domestic capital decides to flee a country in a short amount of time, its balance of payment may be disrupted and its financial stability compromised.

2. Asset price fluctuation

A less direct but probably more fundamental shock is asset price fluctuation as a result of capital flight. Given that leverage typically increases significantly when the Federal Reserve cuts interest rates and the global cost of financing decreases, sudden cost increases in financing and shortage of domestic capital would cause both corporate earnings and asset prices to drop substantially.

Chinese Bank Loans 200 Million And Takes Full Exclusive Fishing Rights Over The Coast Of Somalia

Such depressed asset prices will cause not only the level of indebtedness to rise rapidly, which further increases a country’s debt burden, but also impairs the asset quality of a country’s financial institutions, which typically have large risk exposure to fluctuations.

3. Currency devaluation

Finally, increasing uncertainty regarding capital flight and domestic financial stability sometimes feeds back to the devaluation of the home country currency, which would further exacerbate capital flight and asset price depreciation.

In the past, similar trouble has led some emerging economies to substantially devalue their currency exchange rate. Others have instead chosen to default their debt, something that drastically increases the country’s borrowing costs in the future, causing an inability to refinance and the possible eventual collapse of its financial system.

Despite some such patterns emerging recently, it is important to keep in mind that history seldom repeats itself. For one, the global economy has sailed through uncharted water for quite some time since the start of the asset purchase programmes (quantitative easing) by the US Federal Reserve after the 2008 global financial crisis.

Similar programmes by other leading central banks have provided so much liquidity to the global economy that even the ending and gradual reversal of such vast asset purchase plans may not hurt the baseline of global liquidity and asset prices as previous interest rate hikes did. After all, rising tides lift all boats; global liquidity will remain at historically high levels even after interest-rate increases.

The flip side of this argument, however, is that given that global investors have been used to such easy monetary policy and excessive liquidity conditions for so long, any unexpected acceleration in the interest rate hike cycle runs great risk of dousing investor sentiment and disrupting global financial markets.

Of course, the exact outcome of a country’s debt situation greatly depends on the economic conditions and preparedness in each. After the 1998 south-east Asian financial crisis and the 2008 global financial crisis, many emerging economies improved greatly in terms of current account surplus and foreign reserve growths. What remains to be seen, however, is how far they have gone in terms of engaging in fundamental structural reform; the determining factor in their economic growth sustainability and resilience.

For example, as the largest emerging economy, China’s situation has shifted dynamically over the past decade. The size and impact of its economy increased tremendously after the 2008 global financial crisis, which set some a very successful example to other emerging economies and provided much-needed growth impetus to the global economy.

On the other hand, escalating nationwide leverage, bubble-like real estate prices, increasing incidents of default of publicly traded debts, and collapse of many peer-to-peer (P2P) lending platforms have all attracted attention to the fragility of China’s economic growth and financial system, just like many other emerging economies.

The good news is that China and many other emerging markets have all grown stronger, more experienced and resilient in case another crisis looms around the corner. The new concern is that these emerging economies may have accumulated much more debt than ever before.

Using the example of China again, its national level debt increased from about 160% of GDP in 2008 to over 260% of GDP in 2016. Part of the debt was used to fuel the 2009 4 trillion yuan ($586 billion) fiscal stimulus package that has crucially pulled the economy of China and the entire world out of slowdown and recession in the aftermath of the 2008 global financial crisis.

The longer-term implication is, however, that there is not very much room for China to unleash another huge wave of stimulus as it did in 2009. After all, some of the problems that China and other emerging economies face right now derive precisely from the consequences of the debt they have taken out previously.

In the end, emerging economies have to abandon the short-term debt-fueled growth model and find their own ways to increase labour productivity at a certain point. Only when that happens will emerging economies be able to finally outgrow their reliance on global business cycles and sensitive exposure to interest-rate decisions by the US Federal Reserve.

Source: World Economic Forum